Wall Street cae afectada por los bancos

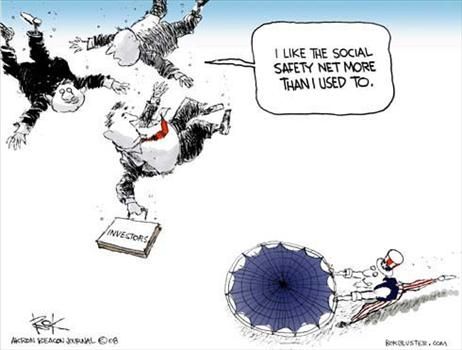

La Bolsa de Nueva York terminó en fuerte baja este lunes, afectada nuevamente por el sector financiero, luego de un inquietante informe del Fondo Monetario Internacional (FMI) y la quiebra de dos bancos regionales: el Dow Jones perdió 2,11% y el Nasdaq 2,00%.

El Dow Jones (DJI.NY) Industrial Average (DJIA) bajó 239,61 puntos, a 11.131,08 unidades y el índice Nasdaq (NDX100.NQ), de alto componente tecnológico, descendió 46,31 puntos a 2.264,22 unidades, según cifras definitivas de cierre.

El índice ampliado Standard & Poor's 500 (SP500.CH)descendió por su parte 23,39 unidades, a 1.234,37 puntos (-1,86%).

Descenso generalizado

"El mercado estuvo particularmente afectado por un descenso generalizado de los (valores) financieros, luego de que el FMI recordara que la crisis del inmobiliario está lejos de haber terminado", explicó Gregori Volokhin, de Meeschaert Capital Market.

En un informe sobre la estabilización financiera, la institución constata un deterioro de la calidad de los préstamos inmobiliarios en Estados Unidos y subraya "los temores ligados a las futuras pérdidas de ciertos grandes bancos comerciales", amplificadas por la reciente quiebra de IndyMac.

Aumentando la presión sobre el sector financiero, "dos nuevos bancos declararon quiebra durante el fin de semana", subrayó Frederic Dickson, de DA Davidson.

Nuevas víctimas de los créditos a riesgo "subprime", dos bancos regionales debieron cerrar sus puertas: First National Bank of Nevada, así como su filial californiana First Heritage Bank.

Estas nuevas quiebras elevan a siete el número de bancos en bancarrota en Estados Unidos desde comienzos del año.

Tendencia bajista

El banco Citigroup (C.NY)cayó 7,53%, Lehman Brothers (LEH.NY) 10,44% y Merrill Lynch (MER.NY)11,59%.

También agudizaron la tendencia "resultados de empresas considerados decepcionantes y la revisión de las previsiones del déficit presupuestario para 2009, acogidas de manera negativa", explicó Peter Cardillo, de Avalon Partners.

La Casa Blanca revisó al alza su previsión de déficit presupuestario, que debería alcanzar un nivel récord de 482.000 millones de dólares, contra 407.000 millones previstos antes.

El mercado obligatorio subió. El rendimiento del bono del Tesoro a 10 años bajó a 4,018%, contra 4,111% en la noche del viernes y el de los títulos a 30 años a 4,614%, contra 4,696%. El rendimiento de las obligaciones evoluciona en sentido opuesto a sus precios.

Lugo se reúne con hija del Ché Guevara

ASUNCION --

El presidente electo Fernando Lugo se reunió el lunes con Aleida, hija del guerrillero argentino Ernesto "Che" Guevara para intercambiar ideas sobre el cambio político en Paraguay, tras la derrota del oficialista Partido Colorado con 61 años de hegemonía política.Lugo, además, recibió al teólogo brasileño Leonardo Boff, quien llegó al Paraguay para dictar una conferencia en la Universidad Nacional de Asunción sobre la defensa del medio ambiente, desde la visión teológica.

Aleida, médico de 48 años, quien arribó el domingo, dijo en conferencia de prensa que fue invitada por Lugo "para charlar sobre los numerosos proyectos que tiene para cambiar al Paraguay".

"No le presenté ninguna propuesta porque él como futuro gobernante tiene su propio plan para todos los sectores pero le hablé de la necesidad de atender prioritariamente a los indígenas desprotegidos, niños pobres que deambulan por las calles y la pobreza en el campo", acotó.

Lugo asumirá el poder constitucional el 15 de agosto.

La hija del ex comandante Guevara, aclaró que "aparte de entrevistarme con Lugo daré un par de conferencias en el sindicato de periodistas y en la facultad de filosofía, de la Universidad Católica, sobre la praxis del cambio político".

Sin embargo, el periodista Enrique Vargas Peña de la radioemisora 9.70, de Asunción, inmediatamente criticó a Eleida "porque cae en una contradicción inadmisible: ¿de qué cambio político hablará si ella sostiene un modelo autocrático, dictatorial o personalista de 50 años de vigencia en Cuba?".

El ex sacerdote franciscano Boff, tras su encuentro con Lugo explicó que "dejaré un mensaje a los estudiantes acerca de los nuevos paradigmas ambientales: el uso racional de los recursos naturales renovables; la educación de niños y jóvenes sobre el manejo ético de la ecología y en especial la naturaleza de la Cuenca del Plata".

"Con Lugo nos conocemos de cuando éramos sacerdotes", expresó Boff a los periodistas. Fue su profesor sobre Teología de la Liberación en los años 80, cuando el futuro presidente era sacerdote.

Agregó que "hoy hablamos de la protección ambiental, específicamente de todo lo que rodea a la represa hidroeléctrica Itaipú, sobre el río Paraná (administrada en sociedad con Brasil)".

Boff dijo estar dispuesto "a colaborar con su gobierno como ecologista... creo que Fernando intentará aplicar en su administración la Teología de la Liberación porque es una opción por los pobres".

Se alzan voces contra proyecto de constitución en Ecuador

Servicios de El Nuevo Herald

La Iglesia Católica expresó el lunes su desacuerdo con el proyecto de nueva Constitución y anunció "una gran catequesis'' para alertar sobre ‘‘inconsecuencias'' respecto al estatismo, al aborto y a la unión entre homosexuales.

"No vamos a hacer una campaña por el 'no'. Vamos a pedir a toda conciencia cristiana que tome nota de las incompatibilidades no negociables de esta Constitución con nuestra fe'', aseguró monseñor Antonio Arregui, presidente de la Conferencia Episcopal Ecuatoriana.

En una rueda de prensa, Arregui difundió las conclusiones a las que llegaron los obispos del país en una asamblea extraordinaria en la que hicieron notar ‘‘inconsecuencias'' en el proyecto de nueva Constitución y detalló las razones del ‘‘desacuerdo'' con su contenido.

Criticó el hecho de que el "estatismo parece ser un hilo conductor'' en la nueva Carta Magna. También cuestionó que "no se reconoce claramente el derecho a la vida desde la concepción'' y se "desdibuja la familia cuando rechaza la existencia de la familia para sustituirla por distintos tipos de familia''.

La propuesta de nueva Constitución redactada por la Asamblea Constituyente y auspiciada por el gobierno será sometida a referendo el 28 de septiembre, cuando los ecuatorianos deben aprobar o rechazar el nuevo texto constitucional.

Arregui apuntó que hay un artículo "ambiguo'' sobre el derecho a la vida y señaló que ‘‘sin mencionar el término 'aborto' el proyecto constitucional deja la puerta abierta a la supresión de la nueva criatura''.

Respecto al artículo de la nueva Constitución que reconoce "la familia en sus diversos tipos'' y admite los mismos "derechos y obligaciones'' de un matrimonio para "dos personas libres'' en unión estable y monógama, Arregui dijo que "una unión entre homosexuales no es familia''.

Sobre el hecho de que desde los púlpitos se está alentando a votar por el 'no', Arregui sostuvo que "nos limitaremos a ejercitar nuestro derecho de libre expresión y de expresión también de nuestra creencia religiosa'' y anticipó que distribuirán la posición adoptada a través de los canales propios de la Iglesia''.

"Ciertamente vamos a hacer una gran catequesis sobre estos valores (cristianos) ... no negociables ... y vamos a tratar de formar las conciencias cristianas en ese sentido. Cada ciudadano será libre de llegar a una conclusión sobre cómo debe votar'', puntualizó.

Mientras tanto, los sectores indígena y sindical de Ecuador anunciaron el lunes que aún no se inclinan por la nueva Constitución, la cual habilitará al presidente Rafael Correa a la reelección hasta mayo de 2013.

"No estamos tan conformes'', expresó el vicepresidente de la Confederación de Nacionalidades Indígenas (Conaie), Miguel Guatemal, y agregó: "lo que queremos es un espacio en el que la reforma sea para todos los sectores''.

"Hace falta planes de desarrollo'', agregó el dirigente, quien tampoco se mostró conforme con la decisión de la Asamblea Constituyente de incorporar a última hora la lengua kichwa (quichua) como oficial de interrelación cultural en la Carta Política que entregó el viernes para el referendo.

"La Asamblea había descartado al kichwa como idioma ancestral'', señaló Guatemal.

Por su parte, el presidente de la Frente Unitario de Trabajadores (FUT), Mecías Tatamues, sostuvo que la nueva Carta Magna --de 444 artículos frente a los 284 de la Constitución que está en vigencia desde junio de 1998-- "es un avance en el país, pero ese avance no se dónde vaya a quedar''.

"Es tan grande, y por eso para leerla va a ser bien complicada y bien duro'', dijo el titular del FUT, que agrupa a las principales centrales sindicales del país.

Los indígenas y los trabajadores indicaron que revisarán la Constitución para definir si votan por el Sí o el No después de dos meses.

La Constituyente, dominada por el oficialismo, aprobó el texto constitucional en medio de las críticas de la oposición, la cual lo califica de "hiperpresidencialista'' y de pretender concentrar todos los poderes en Correa.

"La Constitución, como está en la parte orgánica del poder, es mentirosa y fascista'', declaró a su vez el ex asambleísta León Roldós, de oposición moderada, y añadió que el documento presenta vacíos en los temas de propiedad, comunicación, transparencia y procesos constitucionales.

Correa anunció que respetará "la decisión de ese pueblo sabio y profundo'' en el referendo y retó a sus adversarios a demostrar las denuncias.

"¿Dónde está el supuesto hiperpresidencialismo? ¿Dónde está la acumulación de poder en el presidente o la Constitución supuestamente hecha a la medida?", expresó el mandatario.

Chávez acusa a Bush de 'revivir la Guerra Fría' en carta a Fidel Castro

- Partidos oficialistas critican el ultimátum lanzado por Chávez a sus aliados

- Chávez bate récords en diez años de gobierno

- Empresas deberán transferir tecnología al gobierno venezolano

- Colombia apuesta a la 'transparencia' del presidente venezolano

- Chávez acusa a aliados de dividir coalición antes de elecciones

El presidente venezolano, Hugo Chávez, acusó al de Estados Unidos, George W. Bush, de "querer revivir la Guerra Fría'' y de "un nuevo intento de agresión contra Cuba'', en una carta enviada al ex mandatario cubano Fidel Castro, publicada hoy por medios oficiales de la isla.

''Se está perfilando un nuevo intento de agresión contra Cuba. Y no solo contra Cuba. Venezuela está también en la mira. Para ello, el imperialismo está montando toda clase de provocaciones verbales'', asegura el gobernante.

''Bush, cuando ya le está llegando el inevitable declive, quiere revivir la Guerra Fría. El hecho de que Rusia se haya puesto de pie, tiene a los halcones fuera de sí y pretenden, a través de las trasnacionales de la comunicación, pulsar la tecla del miedo. Y no son gratuitas, en este sentido, las falacias que están fabricando contra Cuba y Venezuela'', agrega Chávez.

Se refiere a un reciente escrito en el que Fidel Castro alabó a su hermano Raúl, presidente de Cuba, por no responder a versiones periodísticas sobre un supuesto plan para instalar una base de bombarderos estratégicos en la isla.

''Estoy completamente de acuerdo contigo -dice-: no tenemos que estar dándole explicaciones ni rindiendo cuentas al imperio yanqui, mucho menos pedirle excusas ni perdón''.

''Frente al imperio y sus amenazas, nosotros debemos fortalecernos'', añade el presidente.

Según Chávez, "otra vez la agresiva obstinación yanqui no solo quiere cercar a la gran potencia que es Rusia (...) sino que busca doblegar, también, a todos aquellos que nos atrevemos a levantar nuestra voz en estos tiempos de genocidio, ensombrecidos por la impunidad''.

Chávez llama "padre y maestro'' al convaleciente Fidel Castro -el sábado se cumplieron dos años de su última aparición en público- y alaba sus columnas de ‘‘reflexiones'', que difunden los medios de comunicación cubanos, todos oficiales.

Esas columnas, según la carta, "son obligada lectura para los revolucionarios y las revolucionarias de nuestra América y del mundo: quien quiera aprehender las líneas de fuerza de nuestro tiempo debe acudir a ellas''.

El mandatario felicita a Fidel Castro por el 55 aniversario del fracasado asalto al cuartel Moncada de Santiago de Cuba, primera acción armada de la revolución contra la dictadura de Fulgencio Batista, que se celebró el sábado.

''Cientos, miles de Moncadas, hemos de seguir tomando por asalto, pero guiados por la nueva experiencia combativa que tiene su más sólido fundamento en los nervios acerados (...) de ello depende esta larga lucha, esta guerra de las contenciones, para doblegar a una fiera cuya mayor debilidad la constituye el dar zarpazos en el vacío'', dice la carta.

Why the global financial turmoil is like an elephant in a dark room

By Martin Wolf

“I was gradually coming to believe that the US economy’s greatest strength was its resiliency – its ability to absorb disruptions and recover, often in ways and at a pace you’d never be able to predict, much less dictate.” Alan Greenspan, ‘The Age of Turbulence’.

We all hope that Mr Greenspan proves right about the US economy. The Federal Reserve’s rate cut on Tuesday will succeed if Mr Greenspan’s view is correct. Yet many fear he is wrong. Many, too, blame him for the current mess. So how did the world economy fall into its predicament?

One view is that this crisis is a product of a fundamentally defective financial system. An email I received this week laid out the charge: the crisis, it asserted, is the product of “greedy, immoral, solely self-interested and self-delusional decisions made throughout the 2000s, and earlier, by very real human beings at the very top of the financial food chain”.

The argument would be that a liberalised financial system, which offers opportunities for extraordinary profits, has a parallel capacity for generating self-feeding mistakes. The story is familiar: financial innovation and an enthusiasm for risk-taking generate rapid increases in credit, which drive up asset prices, thereby justifying still more credit expansion and yet higher asset prices. Then comes a top to asset prices, panic selling, a credit freeze, mass insolvency and recession. An unregulated credit system, then, is inherently unstable and destabilising.

This is the line of argument associated with the late Hyman Minsky, who taught at Washington University, St Louis. George Magnus of UBS distinguished himself by arguing early that the present crisis is a “Minsky moment”: “A collapse of debt structures and entities in the wake of asset price decay, the breakdown of ‘normal’ banking functions and the active intervention of central banks”. This follows an extraordinary dependence on credit growth in the recent cycle (see chart).

Economists would offer contrasting explanations for this fragility. One is in terms of rational responses to incentives. Another is in terms of the short-sightedness of human beings. The contrast is between misdirected intelligence and folly.

Those who emphasise rationality can readily point to the incentives for the financial sector to take undue risk. This is the result of the interaction of “asymmetric information” – the fact that insiders know more than anybody else what is going on – with “moral hazard” – the perception that the government will rescue financial institutions if enough of them fall into difficulty at the same time. There is evident truth in both propositions: if, for example, the UK government feels obliged to rescue a modest-sized mortgage bank, such as Northern Rock, moral hazard is rife.

Yet it is also evident that everybody involved – borrowers, lenders and regulators – can be swept away in tides of all-too-human euphoria and panic. To err is human. That is one of the reasons regulation is rarely countercyclical: regulators can be swept away, as well. The financial deregulation and securitisation of the most recent cycle merely encouraged an unusually wide circle of people to believe they would be winners, while somebody else would bear the risks and, ultimately, the costs.

Yet there is a different perspective. The argument here is that US monetary policy was too loose for too long after the collapse of the Wall Street bubble in 2000 and the terrorist outrage of September 11 2001. This critique is widely shared among economists, including John Taylor of Stanford University.* The view is also popular in financial markets: “It isn’t our fault; it’s the fault of Alan Greenspan, the ‘serial bubble blower’.”

The argument that the crisis is the product of a gross monetary disorder has three variants: the orthodox view is simply that a mistake was made; a slightly less orthodox view is that the mistake was intellectual – the Fed’s determination to ignore asset prices in the formation of monetary policy; a still less orthodox view is that man-made (fiat) money is inherently unstable. All will then be solved when, as Mr Greenspan himself believed, the world goes back on to gold. Human beings must, like Odysseus, be chained to the mast of gold if they are to avoid repeated monetary shipwrecks.

A final perspective is that the crisis is the consequence neither of financial fragility nor of mistakes by important central banks. It is the result of global macroeconomic disorder, particularly the massive flows of surplus capital from Asian emerging economies (notably China), oil exporters and a few high-income countries and, in addition, the financial surpluses of the corporate sectors of many countries.

In this perspective, central banks and so financial markets were merely reacting to the global economic environment. Surplus savings meant not only low real interest rates, but a need to generate high levels of offsetting demand in capital-importing countries, of which the US was much the most important.

In this view (which I share) the Fed could have avoided pursuing what seem like excessively expansionary monetary policies only if it had been willing to accept a prolonged recession, possibly a slump. But it had neither the desire nor, indeed, the mandate to allow any such thing. The Fed’s dilemma then was that the only way to sustain domestic demand at levels high enough to offset the capital inflow (both private and official) was via a credit boom. This generated excessively high asset prices, particularly in housing. It has left, as a painful legacy, stretched balance sheets in both the non-financial and financial sectors: debt deflation, here, alas, we come.

When I read these analyses, I am reminded of the story in which four people are told to go into a dark room, hold on to whatever they find and then say what it is. One says it is a snake. Another says it is a leathery sail. A third says it is a tree trunk. The last says it is a pull rope.

It is, of course, an elephant. The truth is that an accurate story would be a combination of the various elements. Global macroeconomic imbalances played a huge part in driving monetary policy decisions. These, in turn, led to house-price bubbles and huge financial excesses, particularly in securitised assets. Now policymakers are forced to deal with today’s symptoms as best they can. But they must also tackle the underlying causes if further huge disturbances are not to come along. What those responses should ideally be at both national and global levels will be the subject of my post-World Economic Forum column next week.

India

Blast after blast

Another spate of deadly terrorist attacks in India

EVERY six months or so, in recent years, unknown terrorists have exploded crude bombs in India’s cities and trains, and a dozen or more people have been killed. But these mystery killers have now upped the tempo. On Saturday July 26th, and in another bomb-blast the day before, at least 50 people were killed in two Indian cities.

The deadliest attacks were in Ahmedabad, in the prosperous western state of Gujarat, on Saturday. At least 49 people died and some 200 were wounded in around 20 small blasts, which came in two waves. The first hit the city’s crowded market area; the second, 20 minutes later, struck a hospital to which many victims had been rushed. The previous day’s atrocity was less bloody: one person was killed and six wounded by eight explosions in Bangalore, the capital of Karnataka—and the centre of India’s important computer-services industry.

A self-proclaimed Indian terrorist outfit, the “Indian Mujahideen”, claimed responsibility for the Ahmedabad attack. It was reported to have sent an e-mail to several Indian television-news channels shortly before the explosions which read: “Await five minutes for the revenge of Gujarat.” This presumably was a reference to the state’s long history of Hindu-Muslim violence, and, in particular, to a slaughter of over 2,000 Muslims in 2002, in which senior members of the bureaucracy and police allegedly colluded. The killing was a response to the deaths of 58 Hindu activists in a fire on a train, for which Muslims, on slender evidence, had been blamed.

The Indian Mujahideen, or those calling themselves by that name, also claimed responsibility for blasts in Jaipur in May. They killed over 60 people. Indian commentators have been quick to blame Pakistan, or members of its Inter-Services Intelligence (ISI) spy agency, for the attack. They always are. But in the absence, so far, of any evidence to support this claim, it is hard to know how seriously to take it. In Ahmedabad, police responded, as they invariably do, with a hasty round up: of some 30 “suspects”. It would be surprising, on past form, if any is convicted of the crime.

In fact, it is quite likely that the ISI is involved in the killing to some degree. The question is: by how many degrees of separation from it? During a 60-year rivalry, Pakistan has made skilful use of Islamist militants against India, in the contested region of Kashmir, and elsewhere. This must have bequeathed its current spooks a heavy case-load of proven and would-be terrorists, in Pakistan, Bangladesh and many parts of India.

It is almost inconceivable that the ISI is no longer trying to keep tabs on these men. It is also likely that some in its ranks, despite the progress of a four-year effort to make peace between India and Pakistan, want to keep up the fight. But the extent to which they are having their wish seems to be largely a matter of guesswork.

Nonetheless, India has been making some increasingly confident guesses. After a suicide bomber attacked India’s embassy in Kabul last month, killing 41 people, including an Indian diplomat and army general, India’s national security advisor, M.K. Narayanan said: “We have no doubt that the ISI is behind this.”

Meanwhile, the effects of the recent spate of violence are all too concrete. The last round of peace talks between India and Pakistan, which were held in Islamabad in May, a week after the blasts in Jaipur, achieved little. Further bilateral meetings, mainly on trade, will be held this week in Colombo, Sri Lanka’s capital, at an annual regional shindig: a summit of the South Asian Association for Regional Co-operation. But the atmosphere has been tainted.

Among India's senior bureaucrats and soldiers the violence serves to confirm their reluctance to forge closer ties with Pakistan on any level. That is a tragedy, but one that India can afford. For Pakistan, a more fragile place, which faces a much bigger Islamist threat within its own borders, the relative benefits of peace would be greater.

July 28 (Bloomberg) -- Bank of America Corp., Citigroup Inc., JPMorgan Chase & Co. and Wells Fargo & Co. threw their support behind Treasury Secretary Henry Paulson's effort to spur covered bonds as a new source of mortgage financing.

``We look forward to being leading issuers as the U.S. covered bond market develops,'' the banks said in a joint statement in Washington. They applauded Paulson's release today of guidelines for issuers of covered bonds, which detail the types of loans that should go into the securities and how their payments ought to be made.

The banks stopped short of announcing specific plans for issuing the bonds, illustrating how the market may be slow to take off in the U.S. in the aftermath of the mortgage meltdown. Even in Europe, where covered bonds are a market in excess of $3 trillion, investors are shunning the debt amid a collapse in appetite for investments in housing.

``Mortgage-backed securities investors are not in the mood right now to buy bonds with anything less than government backing,'' Kenneth Hackel, managing director of fixed-income strategy at RBS Greenwich Capital Markets in Greenwich, Connecticut, said in a interview, referring to debt guaranteed by Fannie Mae and Freddie Mac.

While the market is ``not yet'' ready for covered bonds, ``the concept is certainly more interesting now than it has been in a very long time,'' he said.

`Ready to Go'

Paulson said the four U.S. banks are ``ready to go'' and that sales by the largest banks can help encourage smaller mortgage lenders to proceed. ``Covered bonds have the potential to increase mortgage financing, improve underwriting standards and strengthen U.S. financial institutions,'' he said.

Covered bonds offer greater protection to investors because banks keep the home loans on their books, and must make up shortfalls if homeowners fail to pay.

The Treasury's guidelines exclude riskier types of mortgages that contributed to the crisis of the past year, including loans made without documenting the borrower's income and those involving higher debt compared with property value.

Paulson said covered bonds will help provide financing to a U.S. mortgage market that now depends on Fannie Mae and Freddie Mac and other government-linked institutions for more than 70 percent of funds.

Fannie, Freddie

Fannie and Freddie slid to their lowest levels in more than 17 years this month on concern they lacked sufficient capital to offset losses and writedowns. That forced Paulson to ask Congress for emergency authority to make equity purchases in them if needed. President George W. Bush plans to sign the bill this week.

Fannie Mae and Freddie Mac buy mortgages and package them into securities sold to other investors. They also borrow to invest in home-loan debt.

Covered bonds achieve higher ratings than regular notes by augmenting the issuer's pledge to pay with a group of assets such as mortgages that can be sold in a default. The extra security allows lenders to pay less interest.

While the securities are backed by loans and bank assets to get AAA ratings, most are valued, on average, as if they were three levels lower.

The Treasury's guidelines spell out a formal definition for covered bonds. The bonds should have maturities of at least one year and no more than 30 years. Home loans in covered-bond pools would have a maximum loan-to-value ratio of 80 percent.

`Paves the Way'

Bank of America Treasurer Jeffrey Brown said in a separate statement that ``today's announcement paves the way to substantial growth in the U.S. market.''

Today's announcement is part of Paulson's strategy of pushing banks to proceed with sales without waiting for legislation to be enacted by Congress. In Europe, which has a covered-bond market of more than $3 trillion, many countries have laws spelling out the ground-rules for issuance.

Federal Reserve Governor Kevin Warsh backed Paulson's plan to support covered bonds, highlighting that the central bank would accept them as collateral at the discount window for direct loans to commercial banks.

``Highly rated, high quality covered bonds would generally fall within that broad range as eligible collateral,'' Warsh said in a statement.

The bonds have been used on a limited scale in the U.S. since 2006, after introductory offerings by Seattle-based Washington Mutual Inc. and Bank of America of Charlotte, North Carolina.

The Federal Deposit Insurance Corp. already has issued new regulations on how covered bonds would be handled in the event of a bank failure. FDIC Chairman Sheila Bair said Paulson's best practices augment the FDIC's efforts to lay out clear guidance for the industry.

``Covered bonds can be a useful tool to help restore confidence and stability to the housing industry, as well as to the mortgage finance system,'' Bair said today.

July 28 (Bloomberg) -- U.S. stocks fell and the Dow Jones Industrial Average lost more than 200 points for the second time in three days after the International Monetary Fund said there is no end in sight to the housing slump.

Merrill Lynch & Co., American International Group Inc. and Fannie Mae led financial shares to a third straight drop as the IMF warned that worsening credit conditions may prolong the economic slowdown. Verizon Communications Inc., the second- largest U.S. phone company, slid to an almost two-year low on a bigger-than-estimated decrease in home-phone lines. Tyson Foods Inc., the second-largest U.S. chicken producer, tumbled the most in six weeks after profit sank 92 percent on higher feed costs.

The Standard & Poor's 500 Index retreated 23.39 points, or 1.9 percent, to 1,234.37, its lowest level since reaching an almost three-year low on July 15. The Dow lost 239.61, or 2.1 percent, to 11,131.08. The Nasdaq Composite Index slipped 46.31, or 2 percent, to 2,264.22. Four stocks fell for each that rose on the New York Stock Exchange.

``We're relatively bearish on financials because even when we get this crisis sorted out, the rebound is going to be muted,'' said Ralph Shive, chief investment officer of 1st Source Corp. Investment Advisors in South Bend, Indiana, which manages $3 billion. ``Everyone wants to declare the crisis over, but it's going to take a long time to dig out of this hole.''

Bearish Forecasts

Half the companies in the S&P 500 that have given outlooks so far say earnings will fall in the third quarter. More than 125 companies in the index report results this week after 236 said second-quarter earnings fell an average 24 percent through July 25.

U.S. stocks dropped last week, resuming a two-month slump, after existing home sales fell more than economists forecast and bond investor Bill Gross predicted $1 trillion of losses for banks and brokerages. All of the 23 developed nations in the MSCI World Index except for Canada experienced bear-market plunges of 20 percent or more since September as credit losses surged and record commodity prices stoked inflation.

The S&P 500 Financials Index lost 4.6 percent today, paring its rebound from a nine-year low on July 15 to 15 percent. The group last week had rallied as much as 30 percent from that low after earnings beat estimates at JPMorgan Chase & Co., Citigroup Inc. and Wells Fargo & Co.

$1 Trillion Prediction

The IMF, which a year ago failed to foresee the depth of the subprime mortgage collapse, stood by its April forecast for about $1 trillion in losses stemming from the U.S. mortgage crisis. While U.S. policy makers have helped contain the financial losses, ``credit risks remain elevated'' and banks need to raise more capital, the IMF said.

Merrill tumbled 12 percent to an almost 10-year low of $24.33, while Lehman Brothers Holdings Inc. slid 10 percent to $15.27.

Lehman had its earnings estimate cut by Merrill analyst Guy Moszkowski, who said the U.S. securities firm may post a further $2.5 billion writedown on home loans in the third quarter.

Bondholders are demanding the highest interest rates for Wall Street debt since 2000, threatening the industry's business model of acquiring assets with borrowed money.

Lehman has seen borrowing costs for its five-year bonds rise to 7.7 percent, up from 5.2 percent six months ago, the biggest jump of the four largest U.S. securities firms, data compiled by Bloomberg show. In some debt maturities, Merrill's bond yields are even higher.

Fannie, Freddie

Fannie Mae lost 11 percent to $10.31, while Freddie Mac retreated 6.7 percent to $7.72. The two mortgage-finance companies may see their equity wiped out if the U.S. Treasury uses new authority to take over the government sponsored companies.

Legislation aimed at shoring up the housing market, passed by the U.S. Senate in a rare Saturday session, is the most comprehensive package considered by Congress to curb a surge in foreclosures, plunging home prices and market turmoil stemming from the worst housing recession since the Great Depression. U.S. foreclosure filings more than doubled in the second quarter from a year ago.

American International Group Inc., the world's largest insurer, slid 12 percent to $23.96 and led the Dow's retreat.

``We cannot see a sustained market recovery unless we have the financials participate or maybe even lead,'' Randy Bateman, chief investment officer at Huntington Asset Management in Columbus, Ohio, said on Bloomberg Television. Huntington oversees $15 billion.

Verizon, Tyson

Verizon lost 2.5 percent to $33.60 even after profit increased 12 percent on higher wireless revenue. Home-phone lines fell 11 percent to 22.4 million. Total phone lines, including business customers, fell 8.5 percent to 38.3 million. High-speed Internet growth also was slower than some analysts estimated.

Tyson slipped $1.14, or 7 percent, to $15.09. The chicken producer said quarterly profit slumped as surging corn and soybean prices boosted the cost of feeding poultry.

Ryanair Holdings Plc. American depositary receipts tumbled 25 percent, leading declines in 13 of 14 companies in the Amex Airline Index, after profit at Europe's biggest discount airline missed analysts' estimates and oil rebounded from a seven-week low. Crude rose $1.47 to $124.73 after Nigerian militants attacked a pipeline.

Amgen Inc., the world's largest biotechnology company, rose the most in the S&P 500, advancing 12 percent to $60.48 after its experimental osteoporosis drug prevented fractures in a trial.

Kraft Foods Inc., the world's second-largest foodmaker, climbed $1.45, or 4.9 percent, to $30.83 after its net income rose for the first time in four quarters, topping estimates. Kraft increased prices on 90 percent of its foods and beverages and shipments fell less than the company expected.

``The market continues to reward those companies that are able to demonstrate strong earnings,'' said Paul Kandel, a money manager at Sentinel Asset Management in New York, which oversees $5 billion.

`Trough'

The bear market in U.S. stocks will probably ``bottom'' in the next month after oil prices fell, Congress passed legislation to shore up the housing market and bank earnings topped estimates, JPMorgan Chase & Co. said.

So-called technical indicators including relative strength indexes, moving averages, short interest and sentiment surveys also signal the S&P 500 won't extend a 22 percent decline from its October record, Thomas Lee, JPMorgan's chief U.S. equity strategist, wrote in a note to clients today.

``Our analysis suggests this low is consistent with a trough,'' wrote Lee, 39, who reiterated his year-end S&P 500 target of 1,450, a 15 percent gain from last week's close. ``We believe equity markets will grind their way higher from here.''

Forecasts In Doubt

The S&P 500 will rise 21 percent from its July 15 low to 1,473 this year, according to the average of nine strategists tracked by Bloomberg. While the index rose 3.5 percent from July 15 to July 25, gains have proved short-lived 10 times during the four U.S. bear markets since 1973.

Predictions that corporate earnings will be the catalyst for a bull market this year are losing credibility as companies make bearish forecasts.

Black & Decker Corp., the largest maker of power tools, cut its 2008 estimate July 25, citing a slump in U.S. homebuilding that is lasting longer than analysts expected. Kimberly-Clark Corp. failed to anticipate pulp and oil costs that were twice its original projection. Of the 63 Standard & Poor's 500 Index companies that provided outlooks this quarter, 30 said profits will fall, data compiled by Bloomberg show.

`Any Excuse'

``Investors are desperately seeking a bottom here and any excuse they can find they're going to declare one, but I don't think we're out of the woods yet,'' said James Gaul, a money manager at Boston Advisors LLC in Boston, which manages $2 billion.

Stocks have declined since October as financial institutions worldwide suffered $468.5 billion in writedowns and credit losses stemming from the collapse of the subprime mortgage market. That prompted economists to forecast 1.5 percent growth in the U.S. economy in 2008, the slowest since 2001. Equities also suffered as inflation increased, giving the U.S. consumer price index the steepest gain since 1991.

The second quarter is poised to mark the fourth straight quarter of declining profits for S&P 500 companies. Earnings have decreased 93 percent at financial firms, 36 percent at companies that depend on discretionary consumer spending and an average 1.2 percent at commodities producers.

Indexes of all 10 industry groups in the S&P 500 have fallen this year, led by a 32 percent tumble in financial shares. Commodities companies have fared the best, dropping 7.2 percent.

In the U.S., Selectively Applied Capitalism

By Steven MalangaThe New York Times recently called the government’s role in propping up Fannie Mae and Freddie Mac “a strange coda” to an era in which U.S. officials, investors and economists often pressed foreign countries to free their own financial institutions from government interference and manipulation even as we turned a blind eye to the growing power and influence of our own quasi-government lending institutions.

In truth, there is nothing strange about it. The U.S. has become a purveyor of what might best be described as selectively applied capitalism, in which we urge free markets and growth policies on the rest of the world but increasingly do not practice what we preach. Today, if you were building a country from scratch you would hardly look to the U.S. as a model of how to tax your businesses and residents, how to regulate your financial systems, or how to use markets and incentives to organize and run government most efficiently.Fannie Mae and Freddie Mac, for instance, didn’t become too big to fail by happenstance. Although the Roosevelt administration created Fannie Mae during the Depression to add liquidity to the mortgage market after lending had dried up, Fannie Mae continued to dominate the secondary market for mortgages long after the credit crisis of the Depression had passed. Rather than wind down Fannie Mae’s role in the mortgage market, in 1970 Congress created Freddie Mac, another government sponsored entity, to compete with Fannie Mae, which had been spun off two years earlier into a quasi-government lender.

Nothing illustrates how difficult it is to end a government initiative, even when its raison d’etre has long passed, than the persistence of Fannie and Freddie. Several studies have estimated that today what Fannie Mae and Freddie Mac give us through their giant borrowing power and implicit government backing (which has recently become explicit) is a reduction in the interest rate on mortgages of about 25 basis points. In other words, the federal government has remained our biggest player in the home mortgage market through these two quasi-public entities for the sake of knocking a quarter of a percentage point off your mortgage.

But this is nothing new and not confined to the mortgage market. Several years ago I attended a conference in Israel on reforming that country’s heavily regulated economy, where I heard a succession of speakers present models of how to reorganize everything from taxes to market regulation. Interestingly, none of the models were based on what we do here in the United States, and I could understand why. Our personal and corporate tax systems and our regulatory regimes are too intricate and burdensome to produce the kind of nimble economy that reformers were seeking.

Our corporate tax rate is now so high and uncompetitive that even re-destributive types like Charlie Rangel, chair of the House Ways and Means Committee, think it should be lowered. Our adjusted federal and average state corporate tax rate, at 39.27 percent, is higher than 28 out of 29 Organisation of Economic Co-operation and Development (OECD) members. In 24 states, including California, New Jersey, Massachusetts, Pennsylvania and New York, the combined federal-local tax rate is higher than in any other OECD country (in 22 OECD countries--including France, Italy, Spain, United Kingdom, Poland and Ireland--there are no state or provincial corporate taxes on top of the federal rate).

Meanwhile, our federal government and the states increasingly see our personal income tax system as a vehicle for achieving social goals instead of principally a method of raising revenue. That has given us a tax system that is not only more progressive but also much more complex than many countries. The country’s top 1 percent of households now earns 21 percent of U.S. income and pays 39 percent of income taxes, according to the Internal Revenue Service. When all income and all taxes are included in the equation, including payroll taxes and the share of corporate taxes paid by individuals, the top 1 percent earns 15.6 percent of income and pays 27.6 percent of taxes, according to the nonpartisan Congressional Budget Office. To achieve these numbers, our federal tax code alone now stretches to more than one million words designed to help politicians underwrite and subsidize everything from mortgages to energy efficiency to college education.

By contrast, 24 countries around the world have now gone in the opposite direction, employing simple flat-tax schemes with no loopholes for special interests and no double taxation in the form of capital gains or estate taxes. Significantly, many of these are former Soviet bloc countries which had a unique opportunity after the fall of the Iron Curtain to design tax systems from scratch. None chose anything remotely like our system, not surprisingly, though many were inspired by ideas they learned here in the U.S., where we talk a good game.

The fall of the Soviet Union has helped spark other free-market changes that have left the United States behind. As markets opened up in many former Soviet bloc countries, our officials, economists and business leaders urged the countries to free their state-controlled enterprises from public control, prompting a wave of privatizations around the world. Looking to rebuild their neglected infrastructures, countries also tapped private markets to finance and operate roads, bridges, airports, water systems and the like. Our Wall Street firms, with the financial expertise to manage these transactions, were happy to lend a hand. In the transportation field alone, some 1,100 privatization deals valued at some $360 billion have taken place over the last two decades--though most were overseas.

Here in the U.S., public sector unions have been effective at fighting privatization and competition for the delivery of public services. Another impediment to free-market reform has been our massive and increasingly corrupt and inefficient system of allowing states to raise money through the use of tax-free municipal bonds. The muni market has been a valuable enabler of corrupt pols, who have plunged states into billions of dollars of debt by using munis to finance pork-barrel projects, non-essential construction like publicly financed stadiums and sports arenas, and public authorities that are managed (and mostly mismanaged) by their patronage appointments. Why tap the private sector when you can ride on the taxpayers’ backs?

This has produced a sharp contrast between how public work is done here and in many other places. In the 1980s, for instance, the Thatcher administration in Britain began a program of contracting with private firms to build and operate toll roads, work continued by the Blair government. A 2002 study in Britain found that whereas 70 percent of publicly managed construction was completed late, and 73 percent came in over budget, only 24 percent of construction managed for government by private firms was late, and 20 percent was over budget. Compare that with the boondoggles produced in places like New York and New Jersey, where giant publicly financed construction authorities, fueled by muni bond offerings, have squandered billions of dollars through fraud, waste and mismanagement.

These days, in other words, we seem to lead only in the amount of energy we expend urging others to do what we don’t do ourselves.

How to Get the Biggest Bang for 10 Billion Bucks

If you had a spare $10 billion over the next four years, how would you spend it to achieve the most for humanity?

This is a small amount compared to rich-government budgets. But if we could set aside an extra $10 billion, we could achieve an awful lot.

![[How to Get the Biggest Bang for 10 Billion Bucks]](http://s.wsj.net/public/resources/images/ED-AH942_lombor_20080727150817.jpg) |

| David Klein |

Would you spend your money tackling diseases like malaria, HIV and tuberculosis, which claim millions of lives each year? Would you battle hunger and malnutrition? What about climate change, which many believe is the biggest challenge facing the planet?

To get the most bang for your buck -- and ensure that your generosity does the greatest good for the largest number of people -- you will need to prioritize, weighing up the costs and benefits of different options. Unfortunately, we too often focus on the most fashionable spending options, rather than the most rational. Spending an extra dollar cutting C02 to combat climate change generates less than one dollar of good, even when we add up all the economic and environmental benefits. In contrast, a dollar spent on research and development into cleaner energy technology generates $11 of economic good. If that dollar was spent combating heart disease in the third world, it would achieve more than twice that again.

Copenhagen Consensus commissioned eight of the world's top economists to identify the global challenges that can be solved most cost-effectively. Over the coming weeks, we will be challenging decision makers and opinion leaders to weigh in on this debate. We also encourage you to go to OpinionJournal.com and respond to this article with your own priorities.

But first, our economists describe how much your extra dollar can achieve in a few areas:

TRANSNATIONAL TERRORISM

Terrorism has become one of the biggest fears. Yet transnational terrorists take, on average, 420 lives each year and cause relatively little economic damage.

An extra $70 billion world-wide has been spent annually on homeland security since 2001. Although there has been a 34% drop in transnational terrorist attacks, there have been 67 more deaths, on average, each year.

This hike in the death toll is entirely predictable. Terrorists have responded rationally to the higher risks imposed by tougher security measures and shifted to fewer attacks that create more carnage.

Increased counterterrorism measures often simply transfer terrorists' attention elsewhere. Installing metal detectors in airports in 1973 decreased skyjackings but increased kidnappings. Fortifying American embassies reduced the number of embassy attacks, but increased the number of assassinations of diplomatic officials. Since counterterrorism measures were increased in Europe, the U.S. and Canada, there has been a clear shift in attacks against U.S. interests to the Middle East and Asia.

Politicians who choose to make counterterrorism a priority have stark options. Spending ever more money making targets "harder" is an easy choice for politicians -- although it will do little to genuinely reduce the terrorist threat.

Increasing defensive measures world-wide by 25% would cost at least $75 billion over five years. In the extremely unlikely scenario that attacks dropped by 25%, the world would save about $21 billion. That figure is reached by adding up the economic damage caused by terrorists, and by putting a high economic value on the lives lost.

But even in this best-case scenario, the costs will be at least three times higher than the benefits. Put another way, each extra dollar spent increasing defensive measures will generate -- at most -- about 30 cents of return.

We could save about 105 lives a year, globally. There are few areas where we would consider spending so much to do so little. To put this into context, 30,000 lives are lost annually on U.S. highways.

Fostering greater international cooperation to cut off terrorists' financing would be relatively cheap and quite effective. This would involve greater extradition of terrorists and clamping down on the charitable contributions, drug trafficking, counterfeit goods, commodity trading, and illicit activities that allow them to carry out their activities.

While this approach would do little to reduce the number of small events, such as "routine" bombings or political assassinations, it could significantly impede the spectacular attacks that involve a large amount of planning and resources. But this would be difficult to achieve, because nations jealously guard their autonomy over police and security matters. A single noncooperating nation could undo much of others' efforts.

Doubling the Interpol budget and allocating one-tenth of the International Monetary Fund's yearly financial monitoring and capacity-building budget to tracing terrorist funds would cost about $128 million annually. Stopping one catastrophic terrorist event would save the world at least $1 billion. Under these assumptions, this would mean a return of about $9 on each dollar spent.

(Figures based on research by Todd Sandler, University of Texas.)

CLIMATE CHANGE

There is unequivocal evidence that humans are changing the planet's climate. We are already committed to average temperature increases of about 1.1 degrees Fahrenheit, even without further rises in atmospheric carbon dioxide concentration.

The world has focused on mitigation -- reducing carbon emissions -- as its response to this challenge. The Kyoto Protocol was an international attempt to cut back on these emissions, and at the end of 2009 politicians will gather in Copenhagen to discuss Kyoto's successor. Although we don't focus on other possible solutions to this challenge, they do exist.

If mitigation -- economic measures like taxes or trading systems -- succeeded in capping industrialized emissions at 2010 levels, then the world would pump out 55 billion tons of carbon emissions in 2100, instead of 67 billion tons.

This is a difference of 18%; but the benefits would remain smaller than 0.5% of the world's GDP for more than 200 years. These benefits simply are not large enough to make the investment worthwhile.

Spending $800 billion (in total present-day terms) over 100 years solely on mitigating emissions would reduce temperature increases by just 0.4 degrees Fahrenheit by the end of this century.

When you add up the benefits of that spending -- from the slightly lower temperatures -- the returns are only $685 billion. For each extra dollar spent, we would get 90 cents of benefits -- and this is even when things like environmental damage are taken into account.

A continued narrow focus on mitigation alone will clearly not solve the climate problem. One problem right now: Although politicians base their decisions on the assumption that low-carbon energy technology is being rapidly developed, that is not the case. These technologies just do not exist. Wind and solar power are available -- at a high expense -- but suffer from intermittency. Researchers need to develop better ways to store electricity when those renewable sources are offline.

If we took that $800 billion and spent it on research and development into clean energy, the results would be remarkably better. In comparison with the 90-cent return from investing solely in mitigation, each dollar spent on research and development would generate $11 of benefits.

(Figures based on research by Gary Yohe, Wesleyan University, and Christopher Green, McGill University.)

DISEASES

Life expectancy is decreasing in some parts of the world. Ten million children will die this year in poor nations. This figure would be just one million if child mortality rates were the same as in rich countries.

The hurdle is not just poverty -- some poor nations have reasonably good health conditions -- but getting cheap treatment and prevention methods to the Third World. There are many ways that we could spend a little money very wisely to make a big difference.

Some health problems receive a lot of publicity. Investment in other areas we hear less about could make a big difference -- such as heart disease in developing nations. Cheap drugs, widely available in rich countries, can manage two major components of cardiovascular risk: hypertension and high cholesterol levels. Simple drugs can also be highly effective in reducing mortality among the millions of adults world-wide who already have some form of vascular disease or diabetes.

In poor countries, where heart disease represents more than a quarter of the death toll, these cheap drugs are often unavailable. Spending just $200 million getting them to poor countries would avert 300,000 deaths each year. The lower burden on health systems, and the economic benefits, mean that an extra dollar spent on heart disease in a developing nation would achieve $25 worth of good.

Much more could be done to reduce the scourge of communicable diseases. In poor countries, malaria will claim more than one million lives this year -- most of them among children under five. Measures to reduce its transmission are simple: more bed nets, preventive treatment for pregnant women, and more indoor spraying with DDT.

Treating malaria is becoming harder because of growing resistance of the malaria parasite to the cheapest, most common antimalarial drugs. Some poor nations cannot afford the new artimisinin combination therapies that work best, and need financial support.

It makes sense to combine prevention options like bed nets with subsidies on the new treatments for poor nations. Spending $500 million would save 500,000 lives a year -- most of them children.

Each dollar spent on ensuring people are healthier and more productive would generate $20 in benefits.

(Figures based on research by Dean Jamison, U.S. National Institutes of Health.)

HUNGER

The food crisis has reminded us that hunger and malnutrition is a daily reality for many in South Asia and sub-Saharan Africa. Malnutrition in mothers and their young children will claim 3.5 million lives this year. Global food stocks are at historic lows. Food riots have erupted in West Africa and South Asia. Progress is distressingly slow on the United Nations' goal of halving the number of hungry people by 2015.

Individual tragedy and national hardship go hand in hand. Shortened lives mean less economic output and income. Hunger leaves people more susceptible to disease, requiring more health-care spending. Those who survive the effects of malnutrition are less productive; physical and mental impairment means children benefit less from education.

There is an obvious focus in improving the quantity of food consumed in developing countries. But it is also vital to improve the quality of diets, especially for children. Eighty percent of the world's undernourished children are in South Asia and sub-Saharan Africa. There are massive benefits from increasing the micronutrients that are lacking in poor communities' diets.

Providing micronutrients -- particularly vitamin A and zinc -- to 80% of the 140 million or so undernourished children in the world would require a commitment of just $60 million annually, a small fraction of the billions spent each year battling terrorism or combating climate change. The economic gains from improved productivity and a lower burden on the health system would eventually clear $1 billion a year. Every dollar spent, therefore, would generate economic benefits worth $17.

Investing in research to make technological improvements to developing-country agriculture provides the opportunity to improve access to micronutrients. It also reduces the cost of food by increasing the incomes of landless laborers. Biofortification can be achieved through genetic modification, or through other methods. Spending $60 million a year would be enough to develop two staple crops such as rice and wheat fortified with micronutrients for about 40 countries across South Asia and sub-Saharan Africa.

The improved nutrition would lead to higher productivity and fewer health problems. Each extra dollar spent would generate economic benefits worth $16.

(Figures based on research by Susan Horton, Wilfrid Laurier University.)

Finding the most cost-effective ways to tackle the world's problems is no simple challenge and should not be left to professional economists alone. Please go to OpinionJournal.com to add your voices to this important debate about prioritization.

Mr. Lomborg is the director of the Copenhagen Consensus. For more information please visit www.copenhagenconsensus.com.

No hay comentarios.:

Publicar un comentario